Introduction to Debt Consolidation Loans

Debt consolidation loans are financial tools that allow individuals to combine multiple debts into a single loan with one monthly payment. This type of loan can help simplify the repayment process and potentially save money on interest payments.

Benefits of Debt Consolidation Loans

- Lower Interest Rates: Debt consolidation loans often come with lower interest rates compared to credit cards or other high-interest debts, which can lead to significant savings over time.

- Single Monthly Payment: By consolidating multiple debts into one loan, individuals only have to make one monthly payment, making it easier to manage finances and avoid missed payments.

- Improved Credit Score: Making timely payments on a debt consolidation loan can positively impact credit scores by reducing overall debt and demonstrating responsible financial behavior.

When Debt Consolidation Loans are Beneficial

Debt consolidation loans are particularly beneficial for individuals with high-interest debts, such as credit card balances, personal loans, or medical bills. By consolidating these debts into a single loan with a lower interest rate, borrowers can save money on interest payments and pay off their debts more efficiently.

Factors to Consider When Choosing a Debt Consolidation Loan

When looking for a debt consolidation loan, there are several key factors to consider that can greatly impact your long-term savings. Understanding how interest rates, loan terms, and different types of loans work is crucial in making an informed decision.

Importance of Interest Rates

Interest rates play a significant role in determining the overall cost of a debt consolidation loan. Lower interest rates can lead to substantial savings over time, as you will pay less in interest fees. It is essential to compare interest rates from different lenders and choose a loan with the lowest rate possible to minimize your long-term expenses.

Impact of Loan Terms on Long-Term Savings

The term of a loan refers to the time you have to repay the borrowed amount, typically ranging from a few years to several decades. While longer loan terms may result in lower monthly payments, they often lead to higher overall interest costs.

On the other hand, shorter loan terms can help you save money on interest but may require higher monthly payments. Consider your financial situation and goals to determine the most suitable loan term for your needs.

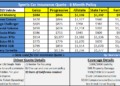

Comparison of Different Types of Debt Consolidation Loans

There are various types of debt consolidation loans available, including personal loans, home equity loans, balance transfer credit cards, and debt management programs. Each type has its own set of advantages and disadvantages, such as interest rates, fees, and repayment terms.

It is essential to research and compare these options to find the best solution that aligns with your financial goals and preferences.

Best Practices for Securing the Most Cost-Effective Loan

When looking to secure a debt consolidation loan, there are several best practices that can help you find the most cost-effective option. By following these tips, you can potentially save money in the long run and achieve financial stability.

Improve Credit Score Before Applying for a Loan

Before applying for a debt consolidation loan, it's essential to work on improving your credit score. A higher credit score can help you qualify for better loan terms, such as lower interest rates. To boost your credit score, focus on making timely payments, reducing debt, and checking your credit report for any errors that need to be corrected.

Shop Around for the Best Loan Offers

Don't settle for the first loan offer you receive. Take the time to shop around and compare offers from different lenders. Look for loans with competitive interest rates, favorable repayment terms, and minimal fees. By exploring multiple options, you can find the best deal that suits your financial needs.

Negotiate Terms with Lenders for Better Deals

When considering a debt consolidation loan, don't be afraid to negotiate with lenders to secure better terms. You can try to negotiate for lower interest rates, reduced fees, or flexible repayment options. Lenders may be willing to work with you to customize a loan that aligns with your financial goals.

Be prepared to discuss your financial situation and demonstrate your ability to repay the loan on time.

Long-Term Savings Strategies with Debt Consolidation

After successfully consolidating your debts, it is essential to have a solid plan in place to maximize your long-term savings. Creating a budget post-consolidation, avoiding new debt, and strategically utilizing the savings from the consolidation are crucial steps to secure your financial future.

Creating a Budget Plan Post-Consolidation for Savings

Once you have consolidated your debts, it's important to create a detailed budget plan that allocates a portion of your income towards savings. Identify your essential expenses, prioritize debt repayment, and allocate a specific amount towards savings each month. This disciplined approach will help you build your savings over time while ensuring you stay on track with your financial goals.

The Importance of Avoiding New Debt While Repaying the Consolidation Loan

While repaying your consolidation loan, it is crucial to avoid accumulating new debt. Taking on additional debt can hinder your progress and lead to a cycle of borrowing that defeats the purpose of debt consolidation. Stay disciplined, stick to your budget plan, and focus on repaying your consolidation loan to achieve long-term financial stability.

Maximizing Long-Term Savings through Debt Consolidation

By consolidating your debts, you can potentially save money on interest payments and streamline your repayment process. Instead of paying multiple creditors with varying interest rates, you can consolidate your debts into a single loan with a fixed interest rate.

This can help you save money over the long term and accelerate your journey towards financial freedom.

FAQ

How can debt consolidation loans help save money in the long run?

Debt consolidation loans can save money by potentially lowering interest rates and simplifying repayment, making it easier to manage debts and reduce overall costs over time.

What factors should be considered when choosing a debt consolidation loan?

Consider factors such as interest rates, loan terms, and types of loans available to ensure you select the most cost-effective option for your financial situation.

Is it important to maintain a good credit score when applying for a debt consolidation loan?

Yes, a good credit score can help you qualify for better loan terms and lower interest rates, ultimately leading to more savings in the long term.

How can individuals maximize long-term savings through debt consolidation?

To maximize savings, individuals should create a budget post-consolidation, avoid incurring new debts, and actively work towards paying off the consolidation loan to reduce overall interest costs.

{kind=link}